Unified Growth Solution

World-class tech needs world-class drivers. AI platform and expert services, unified

Order a free copy of the Positionless Marketing book

Claim your copyRead time 12 minutes

AI in Retail (AI and the future of the retail marketer)

Executive Summary :

Back-to-school shopping in 2026 will be shaped by varied needs, as families are shopping for children across multiple school levels (from pre-kindergarten to high school), and households that often face budget constraints, and problems with product availability.

Consumers are not waiting until late summer to begin. A significant share of shoppers starts before June, while others continue through July and August, making back-to-school a progressive shopping journey rather than a single campaign window. Discounts and promotions remain the strongest incentive to shop earlier, but scarcity, limited availability, and early access to new products also play an important role in pulling demand forward.

For brands and retailers, the main implication is that demand is strong, but shoppers remain under pressure. More than half expect to spend more than last year, yet budget constraints are still the leading concern, and nearly one in six families say they will not be able to get everything they need.

Beyond price, shoppers are also concerned about finding the right sizes, locating specific school supplies, managing multiple lists, avoiding stockouts, and dealing with shipping delays.

Positionless Marketing enables marketers to respond to this complex season in real time. By monitoring behavioral signals, demand patterns, product interest, availability concerns, and household needs, brands can take pre-emptive action. They can personalize offers, manage timing, reduce friction, and deliver the right product, message, offer, and channel experience at the precise moment each family is most likely to act.

Methodology :

Optimove surveyed 648 U.S. consumers in Spring 2026, ages 18+, with household incomes of $75,000+. The analysis in this report focuses on shopping behaviors and attitudes, using both dedicated questions and related cross-survey data on discovery, decision-making, messaging, payments, and multichannel behavior.

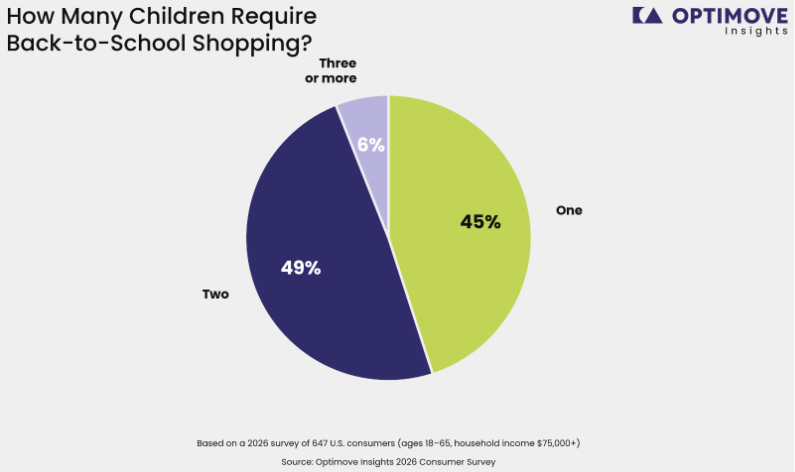

Findings: Nearly half of respondents (49%) are shopping for back-to-school supplies for two children, while 45% are shopping for one child.

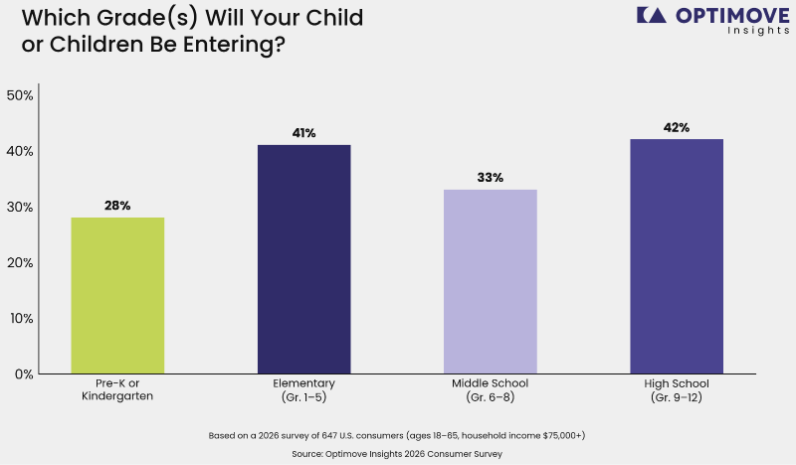

Families are spread across all school levels, led by high school (42%) and elementary school students (41%), followed by middle school (33%) and pre-kindergarten/kindergarten (28%).

Insights: The back-to-school audience is primarily made up of one or two children. The strong presence of both elementary and high school shoppers shows that brands are speaking to families with varied needs, from basic classroom supplies and clothing for younger children to technology, personal care, apparel, and independence-driven choices for older students.

Because many respondents selected more than one school level, the data reveals that some households are shopping across different age groups simultaneously. This makes the shopping needs season more complex: parents may be comparing categories, adjusting spending by child, and responding to different levels of urgency, practicality, and student influence.

How Marketers Should Respond:

Brands should avoid treating back-to-school shoppers as one uniform audience. Messaging, offers, and product recommendations should reflect both the number of children in the household and the school levels represented, helping parents quickly find relevant bundles, lists, and category solutions.

Marketers should use customer data to identify whether a family is shopping for one child, two or more children, or multiple grade levels. The strongest campaigns will make the shopping journey easier by matching offers to household needs, from elementary essentials to high school-ready products, while helping families manage cost, convenience, and timing.

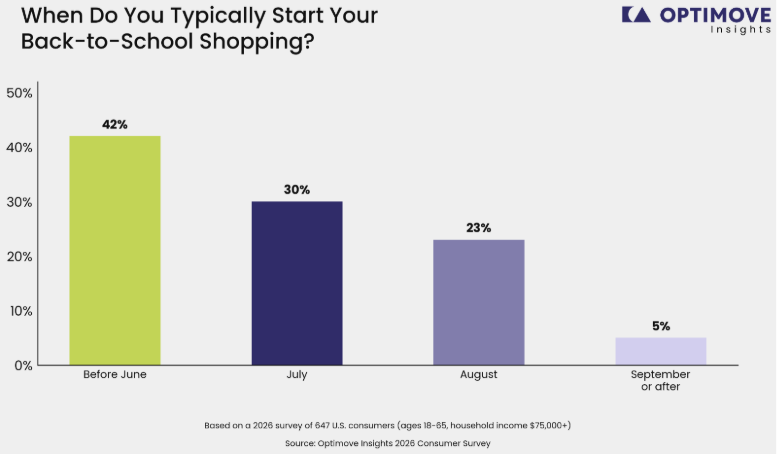

Findings: Back-to-school shopping begins well before the school year for many families: 42% start before June, followed by 30% in July, and 23% in August.

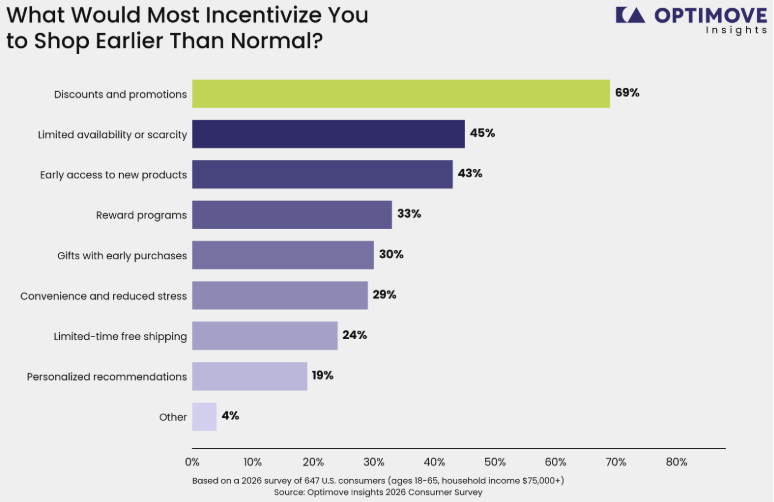

Discounts and promotions are the strongest incentive to shop earlier than usual, selected by 69% of respondents, followed by limited availability or scarcity at 45% and early access to new products at 43%.

Insights: Back-to-school is not a late-summer shopping moment. A large share of families begin preparing before June. It means demand starts building months before the traditional seasonal peak. July and August still matter, but they are part of a longer journey rather than the full campaign window. And July and August are likely times when families add last-minute products, rather than make it the bulk of their shopping journey.

The data shows that early shopping is mainly driven by value and urgency. Discounts and promotions are the most powerful trigger, but scarcity and early product access also play a major role. Families are not only looking to save money; they are also trying to secure the right products before availability becomes uncertain.

This makes back-to-school a progressive buying journey shaped by timing, budget pressure, and product availability. Some shoppers are ready to act early when the offer is strong, while others may wait until the need becomes more immediate. Brands that wait until August risk missing families who have already purchased.

How Marketers Should Respond:

Brands should begin back-to-school campaigns early, using June and even pre-June activity to capture rising intent. Early messaging should focus on value, availability, and planning, helping families feel they are making smart decisions before the season becomes more crowded and stressful.

Marketers should use discounts strategically to pull demand forward, while combining them with scarcity cues, early-access offers, reward programs, and reminders. The strongest campaigns will not rely on one late seasonal push. Instead, they will evolve over time based on when each family is most likely to start shopping and what motivates them to act.

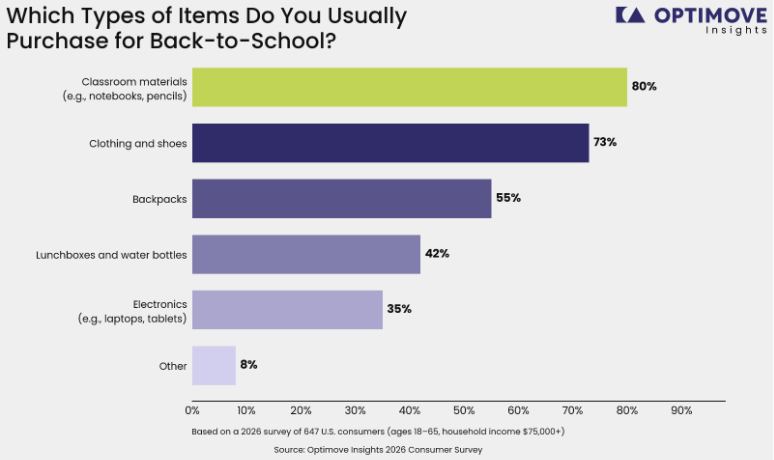

Findings: Classroom materials are the top back-to-school purchase category, selected by 80% of respondents, followed by clothing and shoes at 73%, backpacks at 55%, lunchboxes and water bottles at 42%, and electronics at 35%.

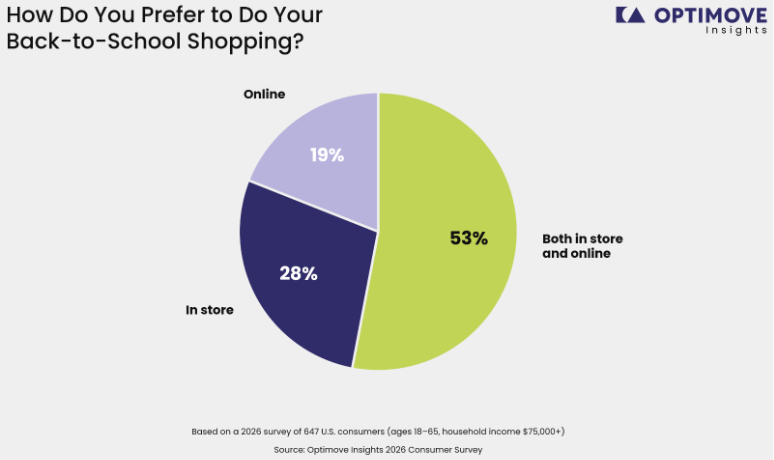

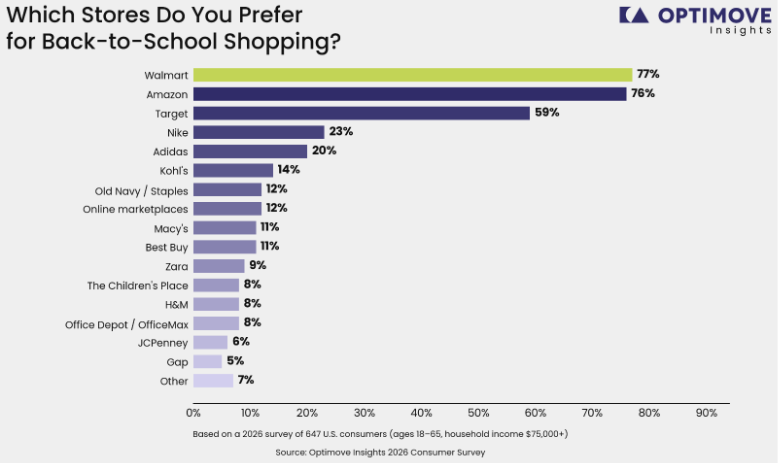

Most shoppers prefer a mixed shopping journey, with 53% buying both in-store and online. Walmart (77%), Amazon (76%), and Target (59%) are the leading retail destinations.

Insights: Back-to-school shopping is built around a practical core basket. Classroom materials, clothing, shoes, and backpacks are the highest-priority categories, showing that families are focused first on the essentials needed to start the school year prepared.

At the same time, the basket extends beyond basic supplies. Lunchboxes, water bottles, and electronics also play an important role, suggesting that families are balancing everyday classroom needs with lifestyle, convenience, and age-specific requirements, especially for older students.

The data shows that families are not choosing between online and in-store shopping as separate paths. Most shoppers prefer to use both, making back-to-school a mixed, multichannel journey where they may browse, compare, validate, and buy across different environments.

Walmart, Amazon, and Target lead because they can support a broad back-to-school mission, while specialty retailers and brands such as Nike, Adidas, Staples, Best Buy, and apparel stores appear more category-specific.

How Marketers Should Respond:

Brands should organize back-to-school campaigns around the full family basket, not isolated products. Messaging should connect classroom essentials, apparel, backpacks, lunch gear, and electronics into clear shopping solutions that make planning easier for parents.

Marketers need to plan for shoppers who move between online and physical touchpoints during the same journey. Families may research online, check availability, visit stores, reorder through marketplaces, or buy different categories from different retailers. The strongest campaigns will keep offers, product bundles, reminders, and recommendations consistent across channels, helping shoppers complete the full mission with less friction.

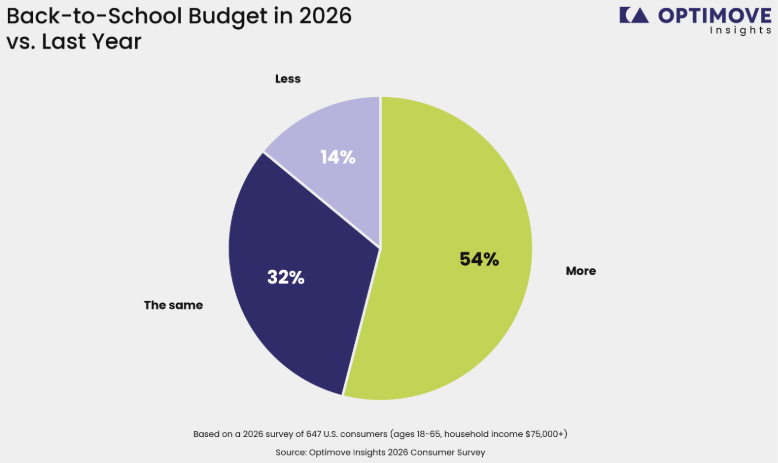

Findings: More than half of shoppers say their 2026 back-to-school budget is higher than last year (54%), while 32% say it is the same, and 14% say it is lower.

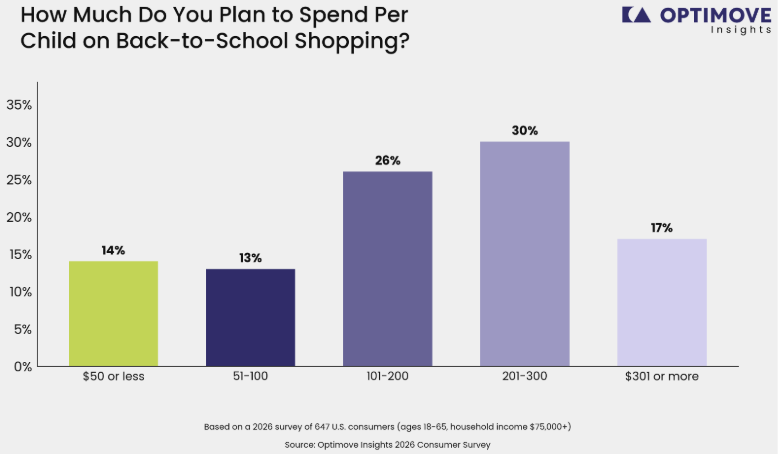

Most families plan to spend between $101 and $300 per child, but budget constraints are the top concern at 55%, and nearly 16% say they will not be able to get everything they need.

Insights: Back-to-school spending is increasing for many families, but that does not mean shoppers feel financially unrestricted. The largest spending groups are concentrated between $101 and $300 per child, showing that families are preparing to spend, but still within clear budget boundaries.

Budget pressure is the main tension of the season. Even as more shoppers expect to spend more than last year, budget constraints rank as the top concern, ahead of sizing issues, finding specific supplies, managing multiple lists, and limited availability. This suggests that higher spending may reflect necessity and rising costs, not only stronger purchase confidence.

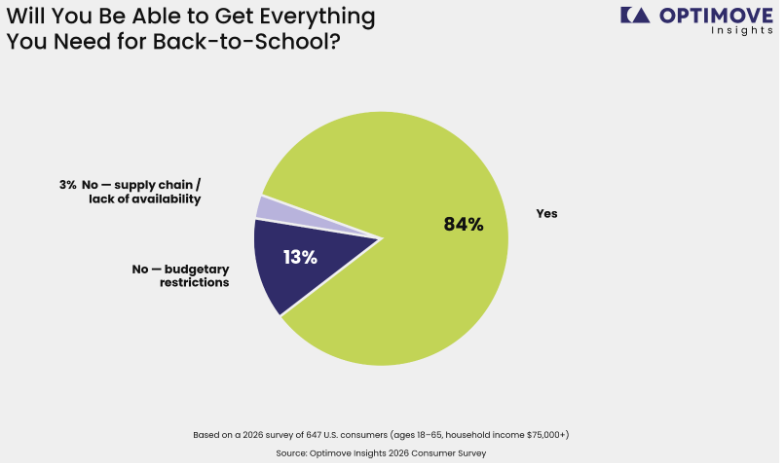

The ability to complete the full back-to-school list is also uneven. While most shoppers expect to get everything they need, about one in six say they will not, mainly because of budget restrictions. For these families, the season is less about choosing between nice-to-have items and more about prioritizing what is essential.

How Marketers Should Respond:

Brands should treat higher back-to-school budgets as a sign of demand, but not as a sign that price sensitivity has disappeared. Messaging should focus on value, durability, bundles, and practical savings, helping families feel that they are stretching their budgets without compromising on what their children need.

Marketers should also identify shoppers showing signs of budget pressure and respond with targeted offers, flexible promotions, reminders, and product recommendations by price tier. The strongest campaigns will help families complete more of their back-to-school lists by making affordability, availability, and relevance work together.

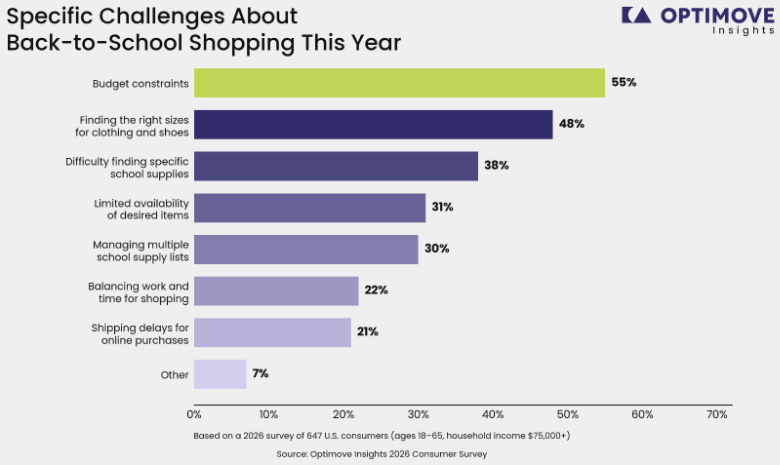

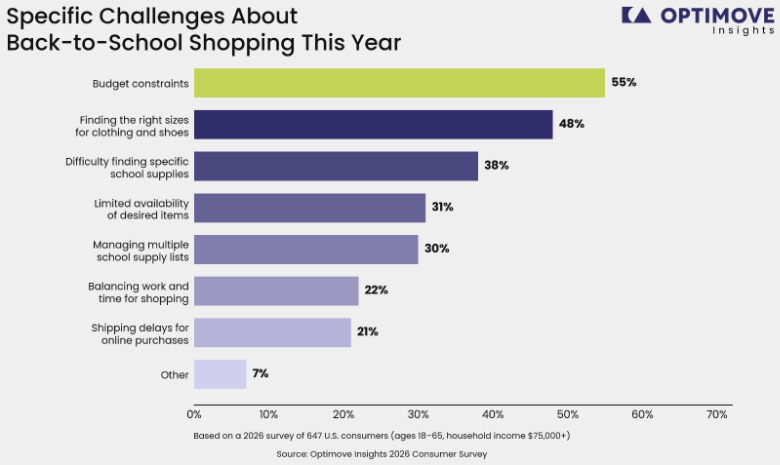

Findings: After budget constraints, the leading back-to-school concern is finding the right sizes for clothing and shoes, selected by 48% of respondents.

Other key challenges include finding specific school supplies at 38%, limited availability of desired items at 31%, managing multiple school supply lists at 30%, balancing work and shopping time at 22%, and shipping delays at 21%.

Insights: Back-to-school friction is strongly connected to whether families can find exactly what they need, when they need it. Concerns around sizing, specific supplies, availability, lists, time, and shipping show that shoppers are looking for certainty throughout the journey.

This creates a major opportunity for retailers to monitor demand and real-time consumer behavior. By understanding what shoppers are searching for, which products are gaining traction, where availability is tightening, and where customers are dropping off, brands can better manage stock, personalize offers, and reduce friction for both shoppers and retailers.

Convenience becomes a strategic advantage when it is built around relevance. Easy returns, extended pickup windows, list-management tools, inventory visibility, and reliable delivery all matter, but the strongest convenience comes from giving each customer the right product, the right offer, and the right reminder at the right time.

How Marketers Should Respond:

Brands should use real-time behavioral data to identify what families need and where friction is appearing. At the same time, real-time shopping data must be in context with historical data to meet the needs of a shopper’s total experience. Campaigns should respond to signals such as size searches, supply-list activity, abandoned carts, product scarcity, delivery concerns, and school-stage needs. Historical data provides context to ensure relevant recommendations, offers, and availability updates.

Retailers should also make convenience a core part of the back-to-school strategy. Flexible returns, longer pickup hours, clear delivery timelines, in-stock messaging, and personalized list support can help families complete the season with less stress. The strongest brands will turn data into action quickly, reducing uncertainty while helping shoppers finish their back-to-school mission.

Back-to-school shopping in 2026 will not be defined by one shopper profile, one purchase moment, or one product category. Families are entering the season with different household structures, school stages, and levels of urgency. The opportunity for brands lies in understanding those differences and supporting the full shopping mission, from early planning to final list completion.

The broader message to brands is clear: back-to-school success depends on moving from seasonal marketing to responsive marketing. Brands that use real-time data in context with historical data to understand what families need, when they need it, and what is blocking the purchase will be better positioned to reduce friction and capture demand. Positionless Marketers can act on those signals quickly, turning insight into personalized campaigns that help families complete the season with less stress and greater confidence.

Optimove, the creator of Positionless Marketing, frees marketing teams from the limitations of fixed roles, giving every marketer the power to execute any marketing task instantly and independently. Positionless Marketing has been proven to improve campaign efficiency by 88%, allowing marketing teams to create more personalized engagement with existing customers.

For two years running, Optimove has been positioned as a Visionary in Gartner's Magic Quadrant for Multichannel Marketing Hubs, recognized for its AI-driven decisioning, prescriptive insights, and proven ability to orchestrate thousands of personalized campaigns in real time across channels.

Its Positionless Marketing Platform includes Optimove Engage and Orchestrate for cross-channel campaign decisioning and orchestration; Optimove Personalize, a digital personalization engine; and Optimove Gamify, a loyalty and gamification platform.

All are powered by Optimove AI, the marketing AI suite that brings AI everywhere marketers work. Inside the platform through Native AI agents for decisioning, analysis, and creation, outside it to external AI tools like Claude and ChatGPT through the Optimove MCP, and into custom-built applications on top of the platform through Optimove Custom Apps. Optimove has embedded AI in its platform since 2012, paving the way for Positionless Marketing.

Today, its comprehensive AI-powered suite is at the leading edge of empowering marketers to streamline workflows from Insight to Creation and through Optimization. Optimove provides industry-specific and use-case solutions for leading consumer brands globally.

Optimove Insights is the analytical and research arm of Optimove, dedicated to providing valuable industry insights and data-driven research to empower B2C businesses.

Agents that let you act while others are still analyzing!