Unified Growth Solution

World-class tech needs world-class drivers. AI platform and expert services, unified

Order a free copy of the Positionless Marketing book

Claim your copyRead time 21 minutes

Part 1: Execution Before, During, and After the Tournament:

The 2026 World Cup Playbook Part 1 shows sportsbook operators how to turn the World Cup from a short-term acquisition surge into sustained player value. It provides practical guidance on pre-tournament cohort preparation, real-time activation during matches, and post-tournament retention of high-value bettors.

Part 2: Global Betting Behavior Ahead of 2026:

The World Cup Playbook Part 2 delivers proprietary, data-backed insight into how football (soccer) betting behavior evolves before, during, and after the World Cup across Europe, LATAM, and the United States. By separating event-driven spikes from durable engagement patterns, it helps operators plan smarter acquisition, retention, and post-tournament strategies.

Terminology Note

“Football” and “soccer” are used interchangeably throughout this report to refer to the same sport.

A practical roadmap for acquiring, activating, and retaining the right bettors before, during, and after World Cup 2026.

The 2026 World Cup will be the largest in history: 48 teams, 104 matches, three host nations, and an estimated 5 billion viewers. For sportsbooks globally, it’s the biggest acquisition opportunity in four years and the biggest retention risk if operators treat it like just another tournament.

For North American operators specifically, this represents something even more significant: the first time the region has hosted since 1994, with matches across favorable time zones and unprecedented local interest. It’s a once-in-a-generation chance to acquire soccer-first fans in a historically under-penetrated market.

The operators who win, regardless of geography, will not only acquire at scale but also activate quickly and retain the right bettors well beyond the final. That

requires treating acquisition and CRM as a single motion, with cohorts and journeys designed before kickoff, real-time operations during the tournament, and a deliberate bridge to year-round betting afterward.

This is an overview roadmap for sportsbooks for the World Cup 2026. Each section will expand into deeper guides as we approach the tournament.

The operators who have already started building cohorts and journeys today will dominate those scrambling in April.

The most effective operators focus their efforts strategically. The whales will bet regardless. The promo-chasers will vanish after the bonus. The target should be

the persuadable cohort in between. This is the segment that yields the highest marketing uplift per dollar spent: the movable middle.

This movable middle clusters into distinct behavioral patterns:

Home-nation patriots follow their country religiously, but go dark after elimination. Operators should plan for this. When Brazil exits in the quarterfinals, or when England’s campaign ends, operators should have a “second team” pivot ready: player-centric narratives, regional favorites, or cross-sport bridges to keep them engaged.

Star-chasers follow marquee players, not countries. They’ll bet on Messi, Mbappé, or Haaland regardless of jersey color. Operators should build journeys around

player props and individual storylines.

Format explorers are new to soccer betting or returning after years away. They need education on rotation risk, draws, and in-play markets. Operators should meet them with simple, low-friction offers and clear explainers.

Operators shouldn’t wait until June to figure out what to say. Teams should build day-0 to day-30 journeys now, including:

• Eligibility rules by cohort and jurisdiction

• Suppression lists for high-risk or low-value segments

• Holdout groups by default to prove lift, not just activity

• Match-day cadences that respect quiet hours and Responsible Gaming rules

Each persona should be mapped to messaging, education, and frequency, so nudges form habits without creating marketing fatigue.

With 48 teams across three host countries and multiple time zones, logistics matter differently depending on where customers are located:

For operators in the Americas: Matches align with prime viewing hours. Communications can run in real-time with local broadcast windows.

For European operators: Many matches will be in the afternoon or early evening local time. This creates opportunities for second-screen engagement during work hours or early evening.

For Asian and Australian operators: Time zone challenges require pre-match education and outcome-based triggers rather than real-time engagement. The focus should be on building anticipation before matches and celebrating results after.

• Localize content for their home markets

• Build match-day triggers that fire at appropriate local times

• Include “dead-rubber” rules (where the outcome doesn’t affect tournament standings or qualification, essentially a meaningless game) so promotions aren’t wasted when group outcomes are already decided

Operators should assemble a ready-to-launch library of journeys and triggers:

• Pre-match education for casual bettors

• In-play prompts tied to game state (goals, red cards, halftime)

• Post-match reactivation for winners and near-miss losers

• Elimination pivots for fans whose teams exit

These should be treated as modular templates, not one-off campaigns. Speed matters more than perfection.

Every market has different opportunities during the World Cup 2026:

North American operators have a once-in-a-generation chance to acquire soccer-first fans during a home tournament. They should plan explicit handoffs to MLS, Liga MX, Champions League, and cross-sport bridges to NBA, NFL, and MLB.

European operators can deepen engagement with existing football fans and cross-pollinate to domestic leagues (Premier League, La Liga, Serie A, Bundesliga) that kick off in August, plus the Champions League starting in September.

Asian and Australian operators can leverage strong diaspora connections and established football fandom. They should bridge to the Premier League, Champions League, and region-specific sports like cricket, badminton, or esports.

Latin American operators benefit from intense home-nation passion. They should bridge to Copa Libertadores, domestic leagues, and leverage regional rivalry narratives that extend beyond national teams.

Operators should track these metrics now to establish baselines before the chaos starts:

• Registration-to-deposit rate

• Day-7 active rate

• Time from brief to live (median and p90)

• Projected LTV vs CAC by cohort

World Cup 2026 won’t wait for weekly standups. Real-time operations separate winners from laggards.

Operators should create a live dashboard that tracks:

• Engagement by time zone and market

• Home-nation vs star-player betting volume

• Promo ROI and redemption rates

• Fatigue signals (declining open rates, unsubscribes)

• Responsible Gaming flags (frequency, loss rates, self-exclusion requests)

This pulse should be used to reallocate spend, adjust frequency caps, and tune eligibility in real-time. Operators without real-time dashboards should prioritize building this capability now. It’s table stakes for 2026.

As lineups rotate and casuals discover rotation risk, operators should:

As lineups rotate and casuals discover rotation risk, operators should:

• Educate bettors on squad depth and lineup uncertainty

• Pivot toward safer or simpler markets when appropriate

• Right-size bonuses to protect margin without killing momentum. Operators shouldn’t assume knowledge. Format explorers need handholding.

When a national team exits, operators have 48 hours to pivot or lose that bettor. They should detect elimination events and shift quickly, focusing on:

• Player narratives: “Follow Messi/Mbappé/Haaland regardless of jersey”

• Underdog stories: “Morocco’s Cinderella run” or “Costa Rica’s giant-killing”

• Diaspora connections: “Italian-Australians supporting Italy” or “Pakistani-Britons backing England”

• Style of play: “If you loved Japan’s attacking style, you’ll love Spain”

• Revenge narratives: “Back the team that knocked yours out to validate the loss”

• Cross-sport bridges for fans ready to move on

Patriotic bettors don’t have to churn the moment their nation is out if operators give them a reason to stay.

Match days require precision. Operators should build triggers for:

• Goals: celebrate wins, console near-misses

• Red cards: pivot to in-play opportunities

• Halftime: quick turn offers before the second half

• Extra time and penalties: high-engagement moments

Every trigger needs to be clear:

• Eligibility logic (who gets it, who doesn’t)

• Channel choice (push vs SMS vs in-app)

• Frequency rules to stay effective and responsible

Vanity metrics don’t matter. Habit formation does. Operators should measure:

• Second bet within 72 hours

• Weekly active sessions

• Match-day reactivation rate

• Share of live bets

• Parlay discovery rate

• Incremental lift by journey (not just clicks)

• Fatigue rate (unsubscribes, opt-outs)

The tournament ends. Operators’ work doesn’t.

At day-14 and day-30, operators should distinguish stable engagers from obvious promo-chasers:

• Suppress or downgrade promo-chasers to low-cost streams

• Graduate engaged bettors to next-best-sport programs. Operators should be ruthless. Not every signup is worth keeping.

Operators should bridge them to ongoing football content relevant to their market:

• Europe: Premier League (August), Champions League (September), domestic cups

• North America: MLS, Liga MX, Champions League, World Cup 2030 futures

• Asia/Australia: Premier League, Champions League, AFC competitions

• Latin America: Copa Libertadores, domestic leagues, international qualifiers

Operators should bridge them to complementary sports in their market:

• North America: NBA (October), NFL (ongoing), MLB playoffs

• Europe: Cricket, rugby, tennis, domestic basketball leagues

• Asia/Australia: Cricket, badminton, esports, basketball

• Latin America: Basketball, volleyball, baseball, domestic leagues

Operators should use simple education and low-friction offers. They shouldn’t assume bettors know how to bet on these sports.

Operators shouldn’t wait 90 days to check in. They should schedule touchpoints at:

• Day 7: “Miss the action? Here’s what’s next”

• Day 30: “Your next big match is here” (league openers, Champions League, etc.)

• Day 60: Seasonal pivots to complementary sports

• Day 90: Win-back offers for at-risk dormancy

Operators should track:

• Day-30 retention rate

• First bet in a non-World Cup market

• Cross-sport adoption rate

• Reactivation saves (successful win-backs)

• Lifetime Value vs Customer Acquisition Cost trajectory by cohort (cohorts can be World Cup 2026 signups vs regular signups, home-nation patriots vs star-chasers, European customers vs Asian customers, etc.)

Across all phases, these principles separate execution from aspiration:

Focus on the movable middle. This segment yields the highest marketing uplift per dollar in every major sport, not just football.

Treat acquisition and CRM as a single plan. Cohorts and journeys should be designed before the first whistle, not in the heat of the moment.

Measure with holdouts by default. Lift should become the language of decision-making, not vanity clicks or open rates.

Protect trust. Responsible Gaming and jurisdictional rules should be baked directly into templates, eligibility logic, and frequency caps. Compliance isn’t a gate at the end. It’s infrastructure from the start.

Shorten the path from brief to live. Teams should aim for hours, not weeks. Reduce handoffs. Give outcome owners end-to-end responsibility within clear guardrails.

This overview is a starting point. Over the coming months, deeper guides will be published on Before, During, and After the tournament, addressing:

• Cohort design and persona mapping

• Real-time trigger architecture

• Market-specific cross-sport handoff playbooks

• Post-tournament retention strategies

The 2026 World Cup will separate operators who treat major events as acquisition spikes from those who treat them as habit-formation engines. The operators who build now (cohorts, journeys, and measurement frameworks) will still be converting June signups into September revenue and beyond.

The operators who win won’t just capture the moment. They’ll build relationships that last long after the final whistle.

Global soccer betting trends (European football) guiding sportsbook operators worldwide ahead of the 2026 World Cup

The FIFA World Cup is one of the largest global betting events, but its impact on sportsbook performance is neither uniform nor inherently durable. This report analyzes betting behavior before, during, and after the 2022 World Cup across Europe, LATAM, and the United States to understand how global football events influence acquisition, engagement, and retention ahead of the 2026 tournament.

Historically, the World Cup drives sharp, short-term spikes in activity and first-time bettors, but rarely reshapes long-term player loyalty. Mature football betting markets such as Europe show steady, habit-driven engagement with minimal disruption, while LATAM exhibits greater volatility that reflects growth rather than weakness. In contrast, the United States has treated the World Cup as a moment, not a season, with engagement peaking during the tournament and normalizing quickly in favor of domestic sports cycles.

The 2026 World Cup, however, introduces structural conditions that make it meaningfully different from prior tournaments. For the first time, the competition will expand to 48 teams, increasing the number of matches, extending the tournament window, and broadening the range of participating nations. In addition, hosting the tournament across the Americas, including the United States, removes many of the time-zone and accessibility barriers that previously limited sustained U.S. engagement with global football.

These factors create a unique opportunity to deepen U.S. exposure to European football and global betting markets. While history suggests that structural change is not guaranteed, the expanded format, extended duration, and geographic proximity of the 2026 World Cup may allow operators to shift U.S. behavior from event-driven spikes toward more sustained engagement, particularly if activation is aligned with the U.S. sports calendar and followed by deliberate post-event nurturing.

Across all regions, mega-events ultimately reveal market maturity rather than erase regional differences. Acquisition surges often come with lower average deposits, and reactivation spikes tend to fade without continued engagement strategies. Durable retention remains strongest where football betting is already embedded into regular behavior.

As the industry approaches the 2026 World Cup, operators face a strategic choice: treat the tournament as a short-term volume accelerator or use its unique structure as an inflection point to build lasting, region-specific engagement.

The outcome will be determined not during the tournament itself, but by how effectively operators prepare before it and invest after it.

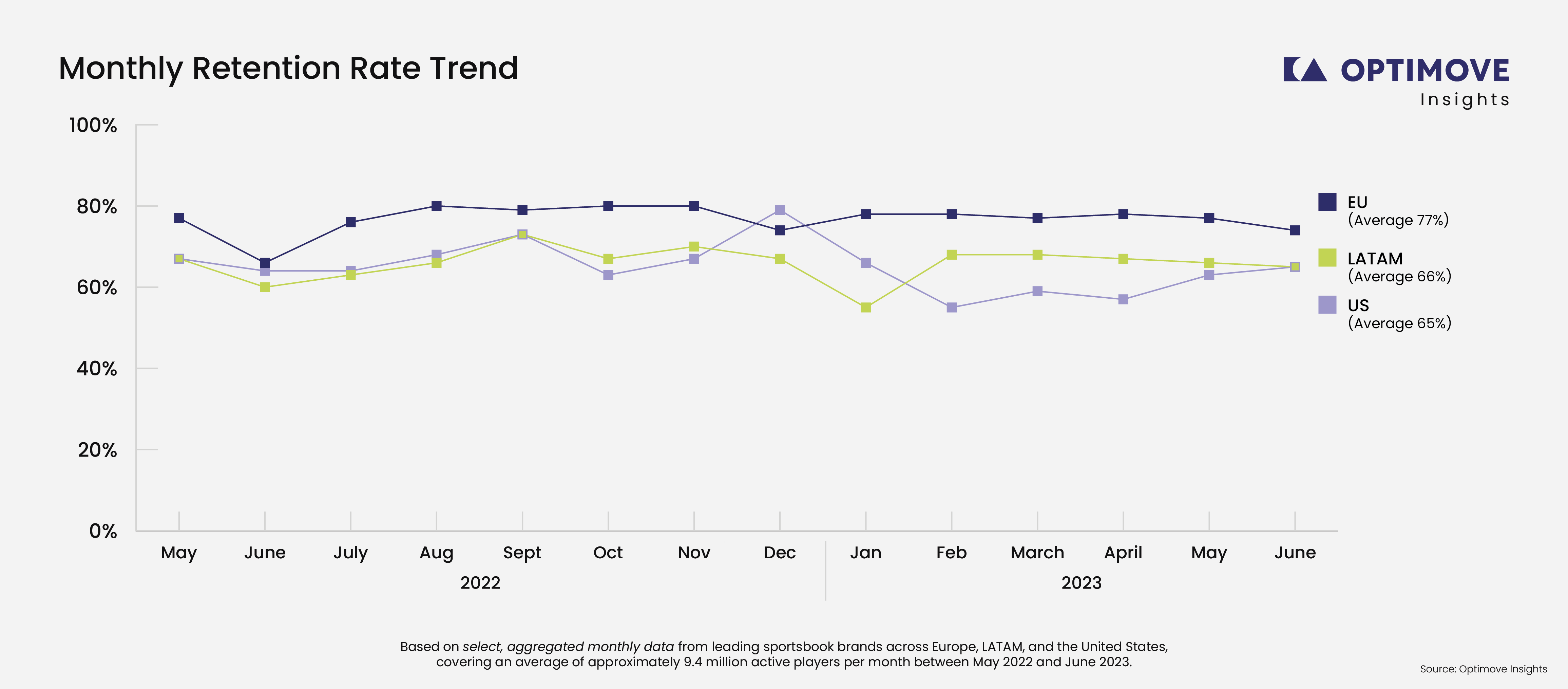

This analysis is based on select, aggregated monthly data from leading sportsbook brands across Europe, LATAM, and the United States, covering an average of approximately 9.4 million active players per month between May 2022 and June 2023. The time period was before, during, and after the 2022 FIFA World Cup. All insights are based on regional-level averages, enabling consistent comparison across markets.

The World Cup creates spikes - not loyalty

Across regions, the tournament drives short-term engagement and acquisition but rarely reshapes long-term player loyalty

Retention is earned before the event, not during it

High-intensity bettors remain loyal regardless of the World Cup, while casual players are far less likely to remain active over time

LATAM’s volatility signals growth, not weakness

The sharp swings in activity and retention reflect a market still forming habits, where global events can temporarily reshape behavior

The U.S. reacts to moments, not tournaments

World Cup engagement in the U.S. is real but short-lived, peaking quickly before giving way to stronger local sports cycles, with little lasting retention effect

Mega-events reveal market maturity

Rather than leveling markets, the World Cup amplified existing structural differences between regions

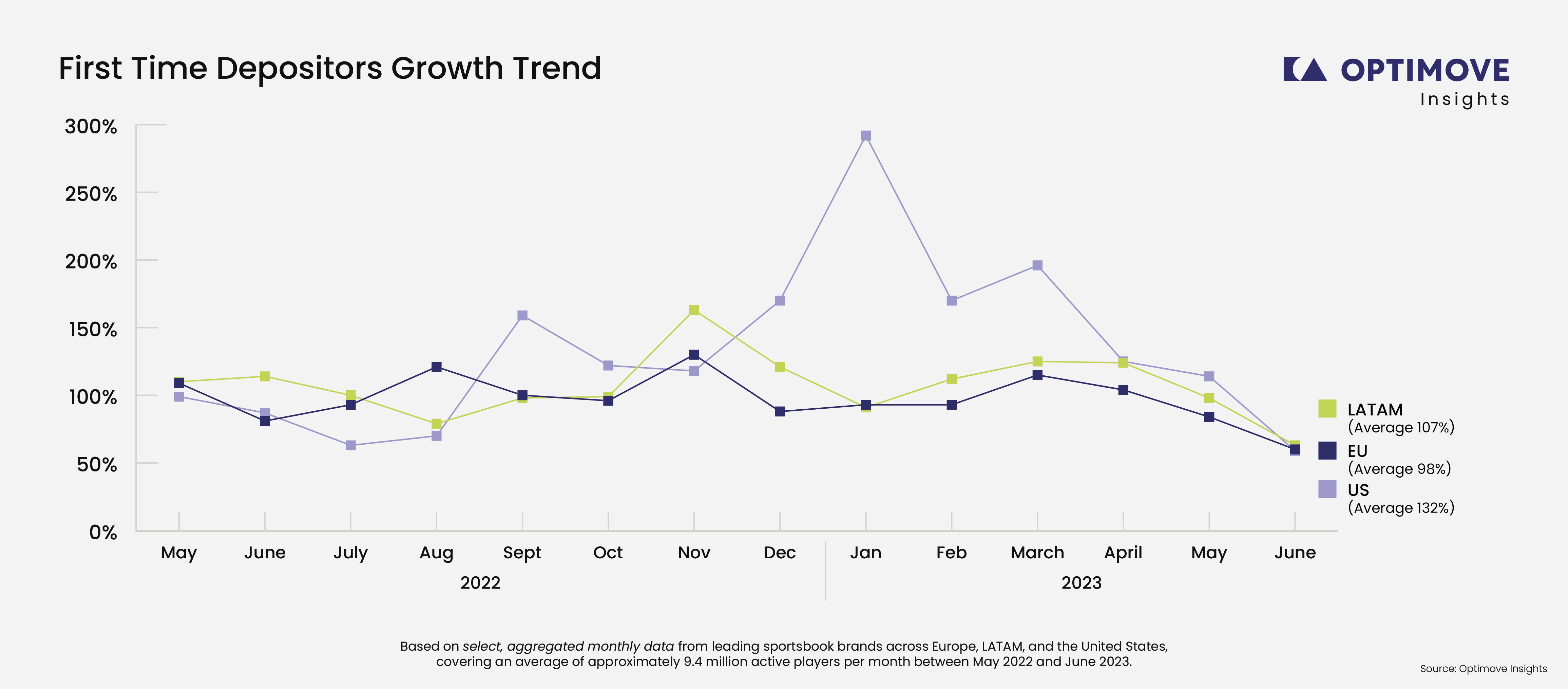

Across regions, first-time depositor behavior around the World Cup showed distinctly different patterns. LATAM demonstrated the strongest uplift, driven by its deeply rooted football culture and the tournament’s outsized influence on new player acquisition. Europe showed a more moderate and predictable increase during the event, reflecting a mature market where soccer betting is already part of the regular cycle. In contrast, the US remained largely unaffected by the World Cup, with no meaningful lift during November–December; instead, its major spike appeared in January, aligned with NFL playoffs rather than global football.

These differences highlight why regional segmentation is essential when evaluating mega-event performance.

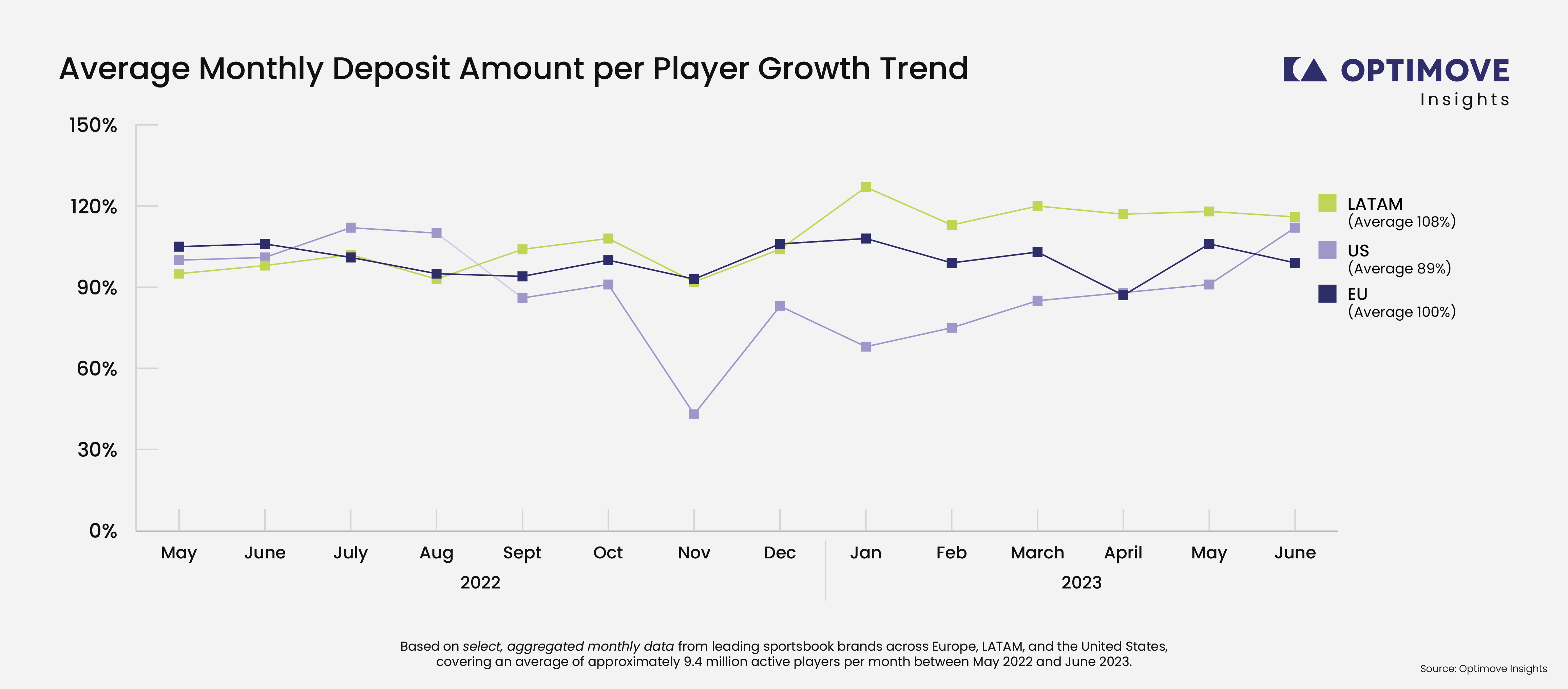

During major global events like the World Cup, growth in player volumes often comes at the expense of average deposit size.

As new bettors enter the market, they typically start with smaller and more cautious deposits. This temporarily decreases the average monthly deposit per player. This effect is most pronounced in LATAM, where football-driven acquisition is especially strong, and the World Cup triggers a surge of low-stakes onboarding. Europe shows a milder version of this dynamic, reflecting a more mature betting market with a relatively stable deposit baseline.

The US follows a different pattern altogether. With football playing a limited role in acquisition, deposit averages dip slightly during the World Cup months but rebound quickly and even rise - once the NFL playoffs (professional U.S. football) begin.

Overall, these trends highlight the trade-off inherent in mega-events: attracting large numbers of new players often means lower short-term value per player, with long-term impact depending on how successfully those players are nurtured post-event.

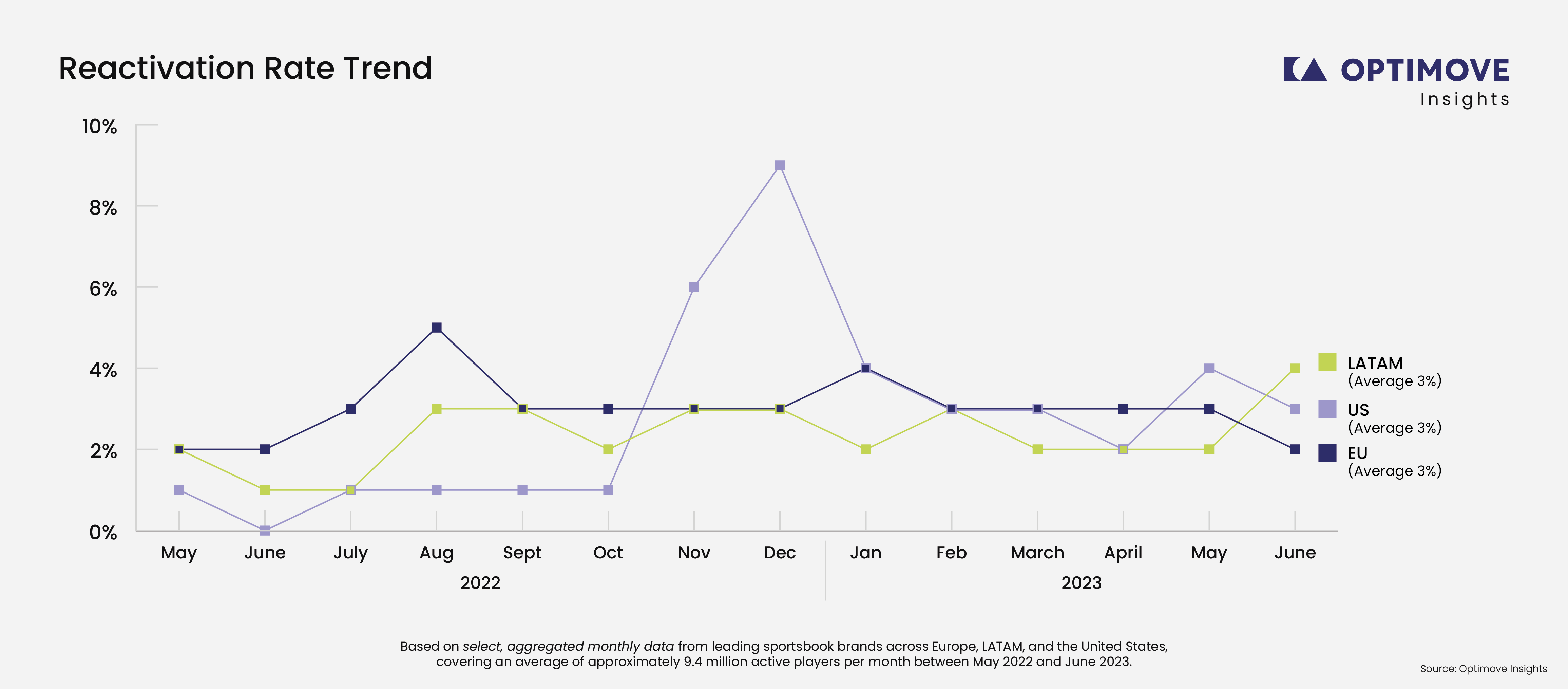

Reactivation behavior during the World Cup reveals clear regional differences in how global sports events re-engage inactive players.

In Europe, reactivation remains relatively stable throughout the period, with only modest fluctuations during the tournament itself. This suggests a mature market where player reactivation is driven more by habitual engagement than by one-off global events.

LATAM shows slightly more movement, with a mild uplift during the World Cup months, but without sharp spikes or sustained post-event momentum. Reactiva-tion here appears responsive to major football moments, yet still anchored in an underlying, steady engagement cycle rather than short-lived surges.

The U.S. stands out with a distinctly different pattern (see more in the special U.S. section of this report). Reactivation rises sharply during the World Cup, peaking in November–December, but drops quickly once the tournament ends. This short-lived spike indicates that while the World Cup can successfully re-engage previously inactive players, it does not create lasting reactivation on its own.

Subsequent activity aligns more closely with the U.S. sports calendar - particularly NFL-driven periods, reinforcing that local sports, rather than global tournaments, remain the primary reactivation drivers in this market.

Summary: Considering all regions covered in this report, these patterns highlight an important distinction: global events like the World Cup can spark reactivation across regions, but the durability of that impact depends heavily on market maturity and the dominance of local sports ecosystems.

Retention trends further emphasize the differences between regions during the World Cup period.

In Europe, retention remains consistently high throughout the year, with only minor fluctuations during the tournament months. Even at peak event periods, player loyalty appears largely unaffected, reinforcing that it is a mature, habit-driven betting base.

LATAM players show slightly higher volatility than Europe. Retention increases toward the World Cup but drops more noticeably in the months immediately following the event, suggesting that while the tournament succeeds in reactivating and engaging players, not all of that activity translates into sustained retention.

The U.S. follows a distinctly different pattern. Retention peaks sharply during the World Cup in December, followed by a pronounced decline in January. This behavior aligns with earlier acquisition and deposit trends, indicating that U.S. player loyalty is far more event-driven and highly responsive to short-term excitement and promotions, but less durable once the event concludes.

Summary: Considering all regions covered in this report, these patterns reinforce a consistent theme across key performance indicator (KPIs): the World Cup amplifies engagement across regions. But engagement only translates into stable, long-term retention in markets with established betting habits like Europe.

As noted, the United States differs structurally from mature European football betting markets. Historically, soccer has not been a primary betting sport in the U.S., and engagement tends to follow the domestic sports calendar more than global tournaments. Established sports betting events in the U.S. are the National Football League (especially the Super Bowl), March Madness, NBA playoffs, World Series, and special annual events like The Kentucky Derby, and College football rivalry games.

Methodology: To help operators anticipate U.S. trends for the 2026 World Cup, we have analyzed betting trends in the U.S. in the previous 2022 World Cup and have analyzed trends in the 2025 U.S. football (soccer). In 2025, the MLS season (soccer/ football) in the U.S. ran from; Start: February 22, 2025, to End (Decision Day): October 18, 2025.

Across major U.S. sportsbook operators, comparing the month prior to the 2022 World Cup with the tournament month, this report analyzed a representative sample of more than 500,000 bettors, who placed up to 18 million bets. In the sample, the following results were revealed:

Despite this surge, U.S. retention and reactivation declined rapidly after the tournament, producing a sharp spike-and-drop pattern on the overlay.

During May 11–June 10, 2025, primarily an off-season period (soccer/football) across the globe:

Soccer betting activity nearly matched U.S. World Cup participation levels from 2022 and exceeded World Cup bet volumes from three years earlier, indicating that soccer betting is increasingly filling seasonal gaps in the U.S. sports calendar.

U.S. versus Europe and LATAM

Compared with Europe and Latin America, the U.S. results reveal:

Strategic Implications for Operators

In the United States:

The 2026 World Cup: Global Expansion, Conditional Impact

The 2026 World Cup introduces unprecedented global conditions:

These factors are likely to increase global betting volume. However, historical data suggests that structural change is not guaranteed. Durable impact will depend on how effectively operators convert event-driven engagement into sustained regional behavior.

Soccer betting is global, but bettor behavior is regional. The World Cup amplifies existing market dynamics rather than reshaping them uniformly.

As the industry approaches the 2026 World Cup, operators worldwide face a clear choice: treat the tournament as a short-term volume spike or use it as a strategic moment to build lasting engagement aligned with regional market realities.

About Optimove

Optimove is the creator of Positionless Marketing and the #1 Player Engagement Solution for iGaming and sports betting operators. Positionless Marketing frees marketing teams from the limitations of fixed roles, giving every marketer the power to execute any marketing task instantly and independently. Positionless Marketing has been proven to improve campaign efficiency by 88%, allowing marketing teams to create more personalized engagement with existing customers.

For two years running, Optimove has been positioned as a Visionary in Gartner’s Magic Quadrant for Multichannel Marketing Hubs, recognized for its AI-driven decisioning, prescriptive insights, and proven ability to orchestrate thousands of personalized campaigns in real time across channels. AI-led marketing is a hallmark of Optimove’s visionary leadership.

By embedding AI directly into its platform as early as 2012, Optimove paved the way for today’s Positionless Marketing standard. Its Positionless Marketing

Platform includes Optimove Engage and Orchestrate for cross-channel campaign decisioning and orchestration; Optimove Personalize, a digital personalization engine; and Optimove Gamify, a loyalty and gamification platform.

Today, its comprehensive AI-powered suite is at the leading edge of empowering marketers to streamline workflows from Insight to Creation and through Optimization. Optimove provides industry-specific and use-case solutions for leading consumer brands globally.

About Optimove Insights

Optimove Insights is the analytical and research arm of Optimove, dedicated to providing valuable industry insights and data-driven research to empower B2C businesses.