Understanding the Differences between Online Casino Gamblers and Social Casino Game Players

The explosive growth of the social gaming market – with 300 million active users per month at Facebook alone (source) – has put this domain on the radar of online casino operators interested in tapping into this trend. On the other hand, because only about 2% of social gamers are paying players, social gaming operators are looking towards the $30.3 billion online casino industry (source) to figure out how to better monetize their player base. In a sound bite: Social games have the reach, while online gambling has the money.

We believe that there is extensive opportunity for these two domains to accelerate each other’s growth. Let’s take a close look at how players differ between these domains and see what implications the differences have.

Research Methodology

Before delving into the data presented here, it’s important to understand the context of where it comes from. We are a software company – our Optimove application helps marketers and retention experts in both online casino and online social gaming companies (among other industries) increase customer spend and lifetime value. Our experience and data in these two fields gives us a deep, unique perspective of the demographics and behavioral patterns of players in both domains.

Please note that all the figures presented here are generalized averages across numerous game types. Despite this, the overall differences in player behavior are very apparent.

Social Gamers are MUCH More Engaged

Our study shows that the level of player engagement in social domains is much higher than in online gambling. A very active social player typically plays every two days, on average, as opposed to a very active gambling player who typically plays once every four days. Thus, active social players exhibit twice the engagement levels!

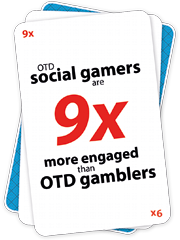

Another interesting fact is that 60% of single-payment social players (known as one-time-deposit, or OTD players, in the gambling realm) will continue to play for fun after their one-time payment.Contrast this with the online gambling space where only 7% of OTD players continue to play after their initial deposit amount is gone. We can thus say that social OTD players are nine times more engaged, since they continue to play even though they do not put any more money into the game.

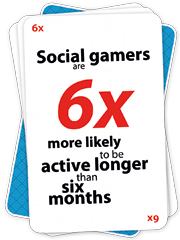

Another important engagement statistic to compare is survival rate, where we see that social gamers are 6.25X more engaged: in social games, 50% of players are still active after six months, as opposed to only 8% in gambling.

There are two main reasons why online social gamers are much more engaged than online gamblers:

More Frequent Interaction

In online gambling, players play via a downloaded PC app or on the website. In order to interact with the game, the player has to specifically go to play, or to receive an email reminding him about the game. In other words, the game is “out of sight, out of mind” most of the time. On the other hand, social games tend to be visible while the player is doing other things in social networks, such as interacting with friends on Facebook. Furthermore, he might be drawn back into the game when seeing his friends playing or after spotting a status message from the app.

Another important factor is the fact that approximately half of social gamers play on their mobile devices, wherever they are, whereas mobile gambling has yet to catch on (possibly because gambling apps are not permitted in the large app stores).

Higher Motivation to Play

In gambling, the player plays to win and to get some kind of a rush. If he wins big, he will usually cash out and might reduce his engagement levels in the near future. In social gaming, there are many more aspects of social/fun engagement which motivate the player. The player wants to compete in the game, to go up in levels, to beat his friends (leader board) and to interact with them by sending gifts.

Proving the impact of the social factor, we have discovered that players with more than a 100 friends are worth 50% more in lifetime value (LTV) terms. When looking at the top social segments (a combination of number of friends, virtual goods sent and messages sent) we see an 80% higher LTV.

The “funs” (non-paying players) database is massive and super important in social because it contributes to the social effect. The fun players are a part of the social ecosystem (I might put in some money in order to beat my fun friends). The social player wants to be virtually rich! Moreover, in social, there is always something happening. You can claim a bonus every few hours. In gambling, if you don’t intend to deposit, you have no reason to come.

Additionally, the perceived value returned by a deposit/payment is often greater in social games: whereas a gambler who loses his money has nothing left, the social gamer may have had a more enjoyable playing experience, reached a higher game level acquired new equipment and so forth.

Beyond Engagement: Other Behavioral Observations

Conversion Rates

We find a huge difference in conversion rates between social gamers and gamblers. In social, the average conversation rate of free players to paying players is about 2%, while in online gambling it is around 18%. This 9X difference is due to the fact that the database of non-paying social players is much larger (there could be millions of MAUs), resulting in a lower conversion rate. In gambling, the player comes to the web site for a specific purpose, he knows why he is there and consequently the conversion is higher (this is related to the platform issue discussed above).

Second-time Depositors (OTD → STD)

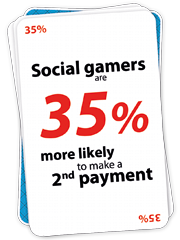

Here, too, there is a significant difference between the two domains. On average, about 62% of social gamers who made a first payment will make a second payment, whereas in gambling it is only around 46%. This 1.35X difference is due primarily to the higher engagement levels in social gaming. Greater engagement means that they are more likely to make another payment while they are involved with the game. Also, social gamers pay for in-game benefits and aren’t worried about “losing” their money whereas gamblers who have lost their first deposit (which they hoped to get back and then some) may be more wary to risk more of their money a second time.

Differences in One-time Deposit and Impact on LTV

Although the average deposit in online gambling is nearly 4X that of social gaming, the average gambler represents an LTV of 2.5X the average social gamer. This indicates that while the average gambler makes larger deposits, the average social player makes more payments.

VIPs

It seems that gambling sites are more dependent on VIPs than social sites. In social, there is also a very strong VIP segment, but the Pareto distribution is not as steep as in gambling. In other words, the top 10% of players in gambling sites generate 80% of the deposits whereas in social, they represent only 60% (25% lower). If you look at the entire Pareto graph you’ll find a smoother, longer tail in social.

Strategic Implications

The fact that there are no withdrawals in social games is what makes it gaming and not gambling. This has an important impact on the level of freedom that marketers have in sending promotions and offers to players: CRM experts can go wild in social because there is no fear of fraud (e.g., using bonus systems to trick the house). Consequently, CRM in social can be used more extensively to engage players and increase their LTV. On the other hand, marketers in social gaming need to prevent game money inflation by offering too much currency.

Another important difference is that social gamers tend to bring in other players more than gamblers do. This is due to both the integral social interaction factor (e.g., group competition, sending gifts to friends) and the relative freedom that marketers have to reward players for getting their friends to join.

Online casino operators may discover that they have a lot to learn from the fun and social “gamification” aspects which are integral to social games. When casino sites figure out how to successfully incorporate gamification aspects such as levels, group competition and social gifting, they can expect to tap into some of the higher engagement and word-of-mouth benefits that social gaming operators already enjoy.

Conclusion

There are extensive and important differences between paying/funded players in the social gaming and online gambling domains. We hope that the data presented in this article can provide deeper insight into the differences between social gamers and online gamblers. Whether or not companies will successfully bridge these two fields is yet to be seen.

Pini co-founded Optimove in 2009 and has led the company, as its CEO, since its inception. With two decades of experience in analytics-driven customer marketing, business consulting and sales, he is the driving force behind Optimove. His passion for innovative and empowering technologies is what keeps Optimove ahead of the curve. He holds an MSc in Industrial Engineering and Management from Tel Aviv University.